Alexander Tsepkov Project Portfolio

Software developer and data geek with 18+ years delivering web, mobile, and defense systems that ship to production. My focus is on analytics platforms, APIs and developer tooling. My open-source work ranges from compilers and automation frameworks to GIS data products. I weave AI-assisted workflows into day-to-day engineering to accelerate delivery and quality.

Is Real Estate Going To Reset in 2026?

Fear sells, especially in real estate. Lately, a number of pundits and headlines have been warning of an imminent housing collapse on par with 2008. One analyst even went so far as to predict a “crash worse than 2008” with home prices potentially plunging 50% starting in 2026. These sensational claims prey on the memory of the last housing bust, but they ignore today’s vastly different fundamentals. The data shows this is not 2008 all over again. If anything, the bigger risk on the horizon is a weakening dollar and easing monetary policy rather than a housing market meltdown.

Fear sells, especially in real estate. Lately, a number of pundits and headlines have been warning of an imminent housing collapse on par with 2008. One analyst even went so far as to predict a “crash worse than 2008” with home prices potentially plunging 50% starting in 2026. These sensational claims prey on the memory of the last housing bust, but they ignore today’s vastly different fundamentals. The data shows this is not 2008 all over again. If anything, the bigger risk on the horizon is a weakening dollar and easing monetary policy rather than a housing market meltdown.

Why 2025 Is Not 2008

The supply situation is the polar opposite of the mid-2000s. In the run-up to 2008, housing inventory ballooned to unsustainable levels, national inventory tripled from 2005 to 2007, flooding the market with a glut of unsold homes and triggering a price collapse. Loose lending meant many of those homes were owned by overstretched borrowers who defaulted en masse. Fast forward to 2025, and inventory is historically tight, not excessive. As of late 2025, active listings remain below pre-pandemic norms, about 6% lower than the same period in 2019. In fact, by some measures housing inventory in 2025 is only ~41% of the 2000–2019 historical average. This scarcity of homes for sale has kept supply far below demand, a key reason we haven’t seen prices plummet even after the pandemic boom.

To quantify this, consider the end of 2025: total U.S. active listings were roughly 1.07 million, about 70,000 fewer homes on the market than at the same point in 2019. That shortfall speaks volumes. Yes, inventory has grown off the absolute lows of 2021-2022 (when active listings nationally dipped under 600k), but it is nowhere near a glut. 2025’s inventory build-up represents a gradual normalization: active listings rose 13% year-over-year, yet were still 6% shy of 2019 levels by year-end. Contrast that with the massive oversupply of 2007.

Lending standards and homeowner profiles are much stronger now. Another huge difference is who owns these homes and how they’re financed. Leading up to 2008, subprime and no-doc loans were rampant; today they’re virtually nonexistent. Banks have spent the last decade tightening underwriting, requiring solid credit, verified income, and reasonable debt-to-income ratios. The result is that the typical homeowner’s balance sheet is far healthier than during the bubble. Back then, Americans’ household debt-to-income ratio soared to ~120% by 2008; now it’s closer to 82%. Most owners locked in fixed-rate mortgages at historically low rates (often under 3%), so they aren’t facing payment shocks and aren’t desperate to sell. There’s no wave of adjustable-rate resets or toxic loans looming over today’s market. Foreclosure activity remains near record lows, because the vast majority of owners can comfortably afford their payments or have substantial equity to tap if needed.

Low inventory and solid loan quality mean prices would rather stagnate than crash. Could home values take a breather or dip modestly in some regions? Sure. Indeed some overheated markets have seen 5–10% corrections. But a 50% nationwide free-fall would require distress on a scale that simply isn’t present. Unlike 2007, when supply overwhelmed demand and credit imploded, today we have an affordability challenge but still an undersupply of homes. As one analysis succinctly concluded, “unlike 2007, where oversupply triggered a price collapse, today’s market is constrained by a shortage of homes”. The power dynamic has shifted slightly toward buyers in 2025, but it’s a measured correction, not a collapse. Even with higher mortgage rates damping demand, multiple offers are still common for reasonably priced homes because there just aren’t enough to go around in many areas. This is not the recipe for a 2008-style plunge.

Perspective Check: Housing Numbers

For anyone feeling flashbacks to 2008, the numbers themselves tell a different story:

- Active Listings: Approximately 1.07 million homes were on the market in November 2025, compared to 1.14 million in November 2019. We are still below pre-COVID inventory levels nationally – whereas 2007 had millions more homes for sale than a few years prior. Today’s buyers actually have fewer options than in a normal market.

- Inventory vs. History: Relative to long-term norms, 2025’s housing supply is extremely tight. By early 2025, active inventory was estimated at only ~41% of the average supply seen from 2000–2019. This is a stark shortage. It’s why even though inventory rose in 2024–2025, national listings were still ~11% below 2019 levels as of mid-2025. Headlines noting “inventory up 30% year-over-year” sound scary until you realize that’s off an abnormally low base, and we’re still nowhere near normal supply.

- Regional Differences: The softening that is happening is very localized. Markets that exploded during the Pandemic (think Phoenix, Austin, Tampa) are the ones finally cooling. As of mid-2025, 12 states – mostly in the Sun Belt and Mountain West – had inventory back to or above 2019 levels. Those were the boomtowns where prices overshot fundamentals. In those areas, it’s true that buyers have more leverage now: Austin and Tampa, for example, saw inventory climb back up and prices come down from their peaks as the frenzy subsided. But even so, we’re talking about moderate corrections (often single-digit percentage declines in home values), not meltdowns. Meanwhile, vast swathes of the country (especially the Midwest and Northeast) still have very tight inventory and even saw modest price gains in 2025.

- Homeowner Equity & Loans: Over 90% of outstanding mortgages carry rates under 5%, and a huge chunk are under 3% from the refinance boom. This locks owners in - they’re not about to panic-sell and give up a 3% loan unless forced. As a result, new listings have been suppressed (“the lock-in effect”), which ironically props up prices by limiting supply. Also, unlike the zero-down days of 2006, today’s buyers typically had solid down payments and have accumulated big equity due to the past decade’s appreciation. With strict lending and negligible subprime exposure, we’re not going to see a flood of foreclosures. Banks and borrowers alike are far more resilient now.

The fundamentals of the housing market in 2025 are nothing like those preceding the 2008 crash. Anyone claiming otherwise is selling fear.

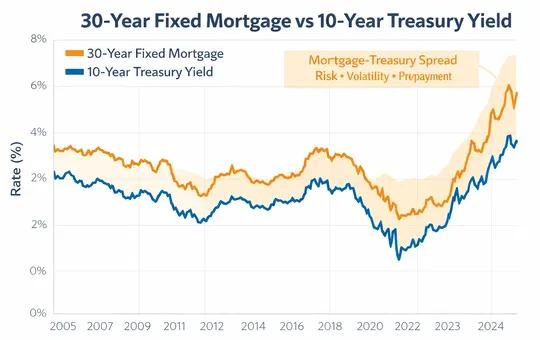

The Real Threat Isn’t Housing, It’s the Dollar

If there’s a “crisis” brewing, it’s not a housing bust. It’s the potential crisis of confidence in our currency and monetary policy. The Federal Reserve has already reversed course from tightening to easing, because the broader economy and financial system can’t handle the previously skyrocketing rates. The Fed just published a report yesterday stating that it cut its policy interest rate (for the third time in a row) down to about 3.5–3.75% and announced an end to quantitative tightening (QT) effective Dec 2025. After a year and a half of aggressive rate hikes and balance sheet runoff, the Fed hit the brakes.

If there’s a “crisis” brewing, it’s not a housing bust. It’s the potential crisis of confidence in our currency and monetary policy. The Federal Reserve has already reversed course from tightening to easing, because the broader economy and financial system can’t handle the previously skyrocketing rates. The Fed just published a report yesterday stating that it cut its policy interest rate (for the third time in a row) down to about 3.5–3.75% and announced an end to quantitative tightening (QT) effective Dec 2025. After a year and a half of aggressive rate hikes and balance sheet runoff, the Fed hit the brakes.

Consider the U.S. government’s debt burden: In FY2025 the Treasury paid $970 billion in interest on the national debt - nearly a trillion dollars burned on interest payments in one year. At 5% rates, the math simply stops working, for the government and eventually for the economy. The Fed knows this. They cannot keep rates high without “drowning” in debt interest and choking off growth. So, whether explicitly or not, they’re being forced to pivot back to an easier monetary stance. The central bank is signaling that the inflation fight is giving way to concerns about financial stability and employment. By the end of 2025 the Fed had already sliced 75 basis points off the peak rates and was expected to cut more in 2026.

Falling interest rates will be a tailwind, not a headwind, for real estate. Mortgage rates tend to follow the 10-year Treasury and Fed policy over time. As investors anticipate the Fed’s U-turn, we’ve already seen mortgage rates dip from their 2023 highs. Lower rates improve affordability and bring sidelined buyers back into the market. In other words, the worst of the affordability crunch may be passing as the rate environment relaxes. Moreover, if the Fed is effectively choosing a bit more inflation (to erode the real value of debt) over crushing the economy, hard assets like real estate become more attractive as an inflation hedge. When the dollar’s value is in question, owning tangible assets (property, commodities, etc.) is often safer than holding cash.

None of this is to say housing is risk-free. Prices in some overheated metros could certainly sag further, and the market is undoubtedly cooler than the frenzy of 2021. But policy makers will likely respond to any serious economic stress by easing (printing money, cutting rates) - which supports asset prices. It’s hard to get a 2008-style crash in that scenario. If anything, the greater danger for homeowners and investors is that high inflation or currency debasement eats away at your savings - another reason real estate (with fixed-rate debt) is a savvy place to be.

Seizing Opportunities During the Lull

Experienced investors aren’t running for the hills; they’re quietly seeing opportunity in the current market. When fear grips the inexperienced, the savvy know it’s time to sharpen their pencils. Personally, I’m using this period of softer demand to buy properties in high-growth markets that were previously too hot to touch. Markets like Austin, Boise, and parts of Florida – which saw explosive pandemic gains – have cooled off just enough to present attractive entry points. For example, as noted, Austin now has inventory back near pre-2020 levels and has seen some price declines. That’s a window for value investors to step in, because the long-term fundamentals (strong job and population growth) remain intact. I’m currently closing on a new construction short-term rental (Airbnb) property in one such market. A year or two ago, it would have been impossible to buy at a reasonable price.